Now sell it for R5000 i.s.o. R1000

Ok. Same scenario as before but now each time we sell it for R5k. I'll just give the net answer in each scenario. The book value at the end of the life is the same as the examples I used earlier but now the company sells it for R5k.

1. NBV = 0; Expense = (R10k); Profit = R5k; Net = (R5k) Loss/Expense

2. NBV = R4k; Expense = (R6k); Profit R1K; Net = (R5k) Loss/Expense

3. NBV = R1k; Expense = (R9k); Profit = R4k; Net = (R5k) Loss/Expense

As I said before, you, like the OP are confused as to what depreciation means and why there is such a concept in accounting.

What matters is cashflows. If the company spends R10k and sells for R5k, the net difference is R5k. Depreciation is a NON-CASH concept (Excl. cash/timing effects of tax consequences). Which means the companies depreciation policy is IRRELEVANT to the buyer of the laptop.

It is economics. The company can ask WHATEVER it wants for the laptop. Anyone with ANY common sense would compare their asking price, against similar laptops with similar specs in order to understand whether or not the laptop is worth the asking price.

Hell the company can have a "perceived value" (@ warwickw) of R10 million for a P4 1.8 Ghz Machine and a book value of R10 million for that machine. If a similar laptop in the market is going for R100, then you would offer at most R100 (barring any other considerations).

Let me give you some insight into accounting... all it is, is an attempt to take information about a business and put numbers to this information in order to make it meaningful.

When a company buys an asset, the reason why it is not an expense is because realistically there is a difference, economically between something that is consumed (E.G. Chocolate/Food) and something that is not consumed, hence despite in both cases cash will flow out, only in the latter is the thing acquired "consumed" immediately and thus an expense.

The rational behind depreciation is to recognise/convey to users of financials, the consumption or use of an asset over time. What benefits can I expect to get from the use of this asset...and when do I expect to receive those benefits.

A laptop is normally used consistantly for a period of time, hence the use of the asset or benefits associated with its use will be earned over time thus the cash outflows are "expensed" consistantly over that period.

Companies are required UPFRONT to ESTIMATE how long they expect to use the asset, and when they are finished with it, what will be the value of the asset. Since it is an estimate, sometimes the estimate is off and you might replace it earlier than expected or later than expected.

@ warwickw: No. Financial decisions are not done based on accounting policy! DO NOT MAKE THIS MISTAKE!

Let me take your example used to make you understand.

End of month 24 (Assuming R10k cost of laptop) means the NBV of the asset will be R5k. Which means for the company not to make an "accounting" loss it would charge R5k. Why? Because if it still estimates it will use the laptop for 2 years, then the company is saying it can still get R5k worth of use of the laptop, it values the benefits of the laptop as being R5k.

Another company might "value" the laptop differently and its value might be more or less, but as the potential buyer I don't care what "value" you have, the question is, is my valuation similar.

From the companies perspective, if they want to suddenly sell the asset instead of use it, they will try and get back what they lose in benefits, but from the buyers perspective it is not relevant.

Stop trying to complicate things. The OP wanted to know what is a "fair" price. Compare the asking price to the "market" price. If the asking price is more, then the company is asking to much for it. If the asking price is less then it could be a bargain.

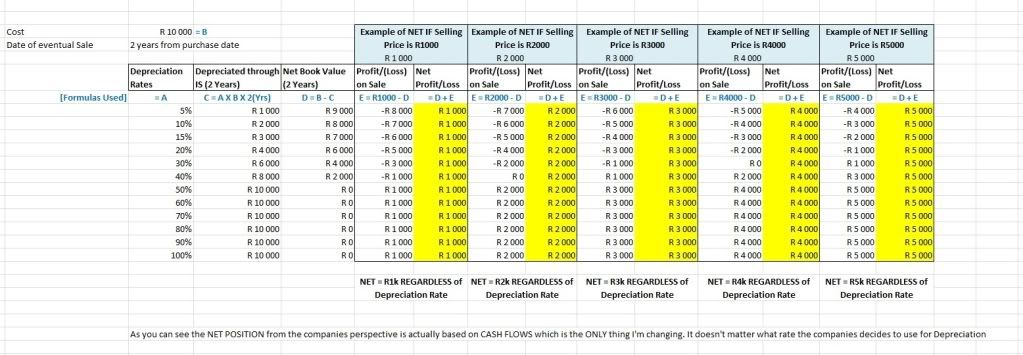

At the end of the day, the depreciation charge is not relevant, the NET answer at the end when the asset is sold will be the same.

See picture for the calcs.

") Just look at other laptops with similar specs and offer the company 80 or 90% of the value you find.

Just look at other laptops with similar specs and offer the company 80 or 90% of the value you find.